Email Us Now: info@fsfinanceltd.com

Bank Guarantees 2026: What Businesses Must Know Before Securing One

As global trade, infrastructure projects, and cross-border financing continue to expand, bank guarantees in 2026 remain a critical financial tool for businesses seeking credibility and risk protection. However, regulations, compliance requirements, and bank expectations have evolved significantly.

Before securing a bank guarantee, businesses must understand how they work, what banks now require, and the risk involved. This guide breaks everything down clearly and practically.

What Is a Bank Guarantee?

A bank guarantee is a financial promise issued by a bank assuring that a beneficiary will receive payment if the applicant fails to meet contractual obligations.

In simple terms, the bank acts as a financial safety net, reducing risk for the party receiving the guarantee.

Common uses include:

- International trade transactions

- Construction and infrastructure projects

- Government contracts

- Equipment leasing and supply agreement

Why Bank Guarantees Still Matter in 2026

Despite the rise of fintech alternatives, bank guarantees in 2026 remain trusted instruments because they are

- Legally enforceable

- Recognized internationally

- Backed by regulated financial institutions

- Often mandatory for large contracts

Banks, however, have tightened issuance standards due to fraud prevention, AML regulations, and capital risk controls.

Types of Bank Guarantees Businesses Use

Performance Guarantee

Ensures the contractor completes a project according to agreed terms.

Payment Guarantee

Assures sellers that payment will be made on time.

Advance Payment Guarantee

Protects buyers when advance payments are made before goods or services are delivered.

Bid Bond Guarantee

Confirms that a bidder will honor the contract if selected.

Key Requirements to Secure a Bank Guarantee in 2026

Banks are far more selective today. Expect the following requirements:

- Strong financial statements

- Verified business registration documents

- Proof of contract or transaction

- Collateral or cash margin (often 30–100%)

- Clear source of funds

- Compliance with AML and KYC regulations

💡 Tip: Shell companies and newly registered businesses face higher scrutiny.

Costs and Fees to Expect

The cost of bank guarantees in 2026 depends on:

- Guarantee amount

- Duration

- Applicant’s creditworthiness

- Risk profile of the transaction

Typical costs include:

- Issuance fee (1%–5% annually)

- Swift messaging fees

- Legal and compliance charges

Higher-risk jurisdictions usually attract higher fees.

Risks Businesses Must Consider

While bank guarantees reduce risk for beneficiaries, applicants should be aware of the following:

- Frozen collateral impacting cash flow

- Automatic payout if terms are breached

- Legal disputes over guarantee wording

- Fraud risks from unverified intermediaries

Always review guarantee terms with a legal or financial professional.

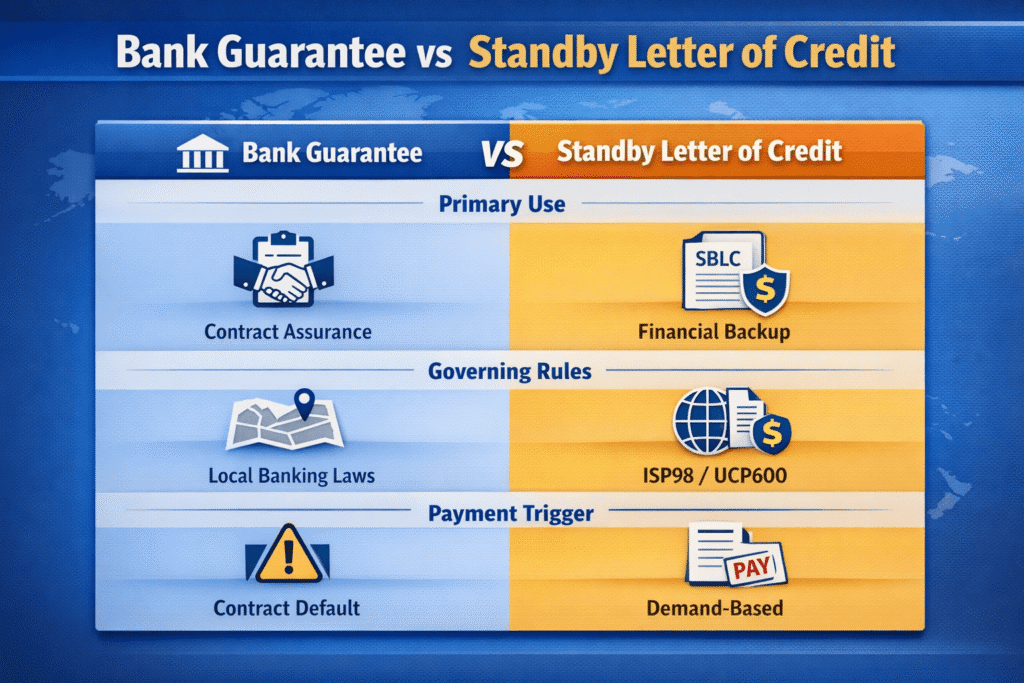

Bank Guarantees vs Standby Letters of Credit

Many businesses confuse these two instruments.

| Feature | Bank Guarantee | SBLC |

| Primary Use | Contract assurance | Financial backup |

| Governing Rules | Local banking law | ISP98 / UCP600 |

| Payment Trigger | Contract default | Demand-based |

Understanding the difference can prevent costly mistakes.

How to Increase Approval Chances

To improve your chances of approval in 2026:

- Maintain transparent financial records

- Work with reputable banks or licensed financial institutions

- Avoid third-party “guarantee sellers” without banking authority

- Ensure contracts are clear and verifiable

Banks prioritize low risk and clarity.

Final Thoughts

Bank guarantees in 2026 remain powerful financial tools, but they are no longer easy to obtain. Businesses that understand the requirements, costs, and risks are better positioned to secure them successfully.

Preparation, transparency, and professional guidance are key to avoiding delays or rejections.